There used to be a time when cash was king for consumers and merchants when transacting business. But things began to change during the 1970s with the explosion of bank and nonbank-issued credit cards. These days, approximately 73% of businesses prefer that customers use cards or apps when making purchases — and most customers prefer to do so anyway, part of the consideration in what’s considered a high-risk merchant.

Consequently, businesses that don’t accept plastic are at a competitive disadvantage and likely to lose substantial sales. This issue can even be more daunting for companies categorized as high-risk entities, as they can face challenges when establishing merchant accounts for processing credit card payments. Continue reading to learn more about what a high-risk merchant account is and how you can find the right payment processor.

What Does High-Risk Merchant Mean?

When a financial institution approves a credit card account for a business, it essentially extends a loan to the merchant, expecting that the company will receive the funds from its customers and cover the credit card payments.

However, in some businesses or industries, there’s a higher likelihood that a merchant won’t be able to process a credit card transaction. When that happens, the bank is on the hook because the buyer’s money for the purchase has already been transferred to the seller’s account and the bank has no way to recover it. Because many financial institutions don’t want to accept the risk, companies often must seek a high-risk merchant account for their payment processing needs.

The following are examples of what’s considered a high-risk merchant :

Alongside being a part of one of the above industries, businesses may be high-risk because of these factors:

Frequent Legislative Changes

Some industries, such as those related to alcohol and firearms, are susceptible to frequent changes in laws and regulations that impact their ability to conduct business. This uncertainty creates a red flag for many financial institutions, as it often leads to instability, higher costs and lower profits.

"Questionable" Products or Services

Part of what’s considered a high-risk merchant has to do with reputation-conscious payment processors refusing to do business with companies because they’re uncomfortable with what they offer. For example, they may refuse to deal with entities that sell adult materials, tobacco, vaping equipment or marijuana paraphernalia.

Limited Experience

Often, banks are leery of working with startups or businesses without an extensive track record. These financial institutions may have concerns about the company’s long-term viability, shortage of resources or lack of experience with payment processing.

Irregular Revenues

Additionally, banks like to see that a company can generate a consistent revenue stream throughout the year before approving a merchant account. Therefore, industries that operate seasonally, such as landscaping, snow removal, outdoor recreation, tax preparation and swimming pool installation and cleaning, may have difficulty opening a merchant account.

Heavy Competition

Many financial institutions view a company attempting to succeed in a saturated market as a high-risk business. These merchants face stiff competition, so the chances of failing are higher. These entities may need to charge lower prices for their products or services to attract customers, which may not generate enough profits to remain viable

Threat of Obsolescence

Continuing advances in technology threaten to put some companies — and even entire industries — out of business. Some payment processors will shy away from an entity in an industry that faces an uncertain future or could be easily replaced by computers or automated processes.

High Chargeback Potential

A chargeback occurs when customers demand that a merchant return their payment for a product or service they’ve purchased by reversing the charge on their credit card. A significant chargeback rate is a warning sign to financial institutions, potentially indicating higher fraud potential. Therefore, banks are wary of businesses with a notable number of chargebacks.

A business that offers free trials or subscriptions that automatically charge credit cards at the end of a designated time frame is more prone to chargebacks. Many customers forget that they signed up for the service and will demand a refund when they become aware of the charge.

Selling High-Ticket Items

Furthermore, companies that offer expensive goods or services for sale may have difficulty obtaining a merchant account. Generally, the more an item costs, the greater the risk of fraud. The buyer’s remorse that may occur when customers realize they paid a lot of money for a product that doesn’t meet their expectations can also contribute to a higher chargeback rate.

Poor Personal Credit

As most small businesses are sole proprietorships or partnerships, the owners must often depend on their personal credit to obtain financing or open a merchant account. If their credit score doesn’t meet a certain threshold, banks will likely classify them as high-risk businesses and reject their application making them what’s considered a high-risk merchant.

Location

Many businesses — especially online entities — that sell their products to U.S. customers have their headquarters in another country. In these cases, banks are often reluctant to set up merchant accounts due to the higher fraud risk. It can also be more challenging to gather reliable information about these organizations during the vetting process.

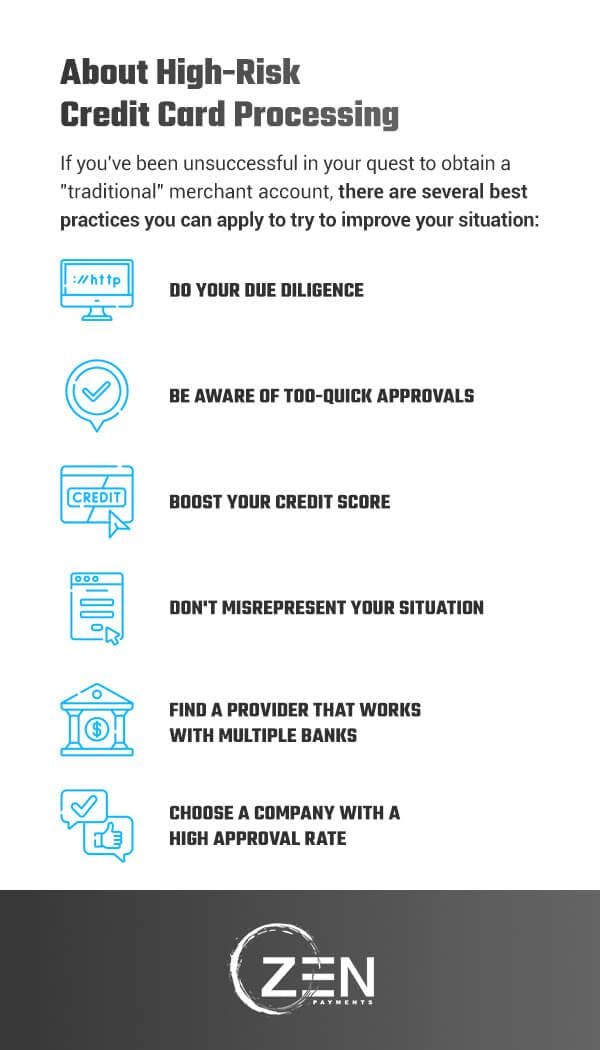

About High-Risk Credit Card Processing

While businesses in the industries listed above — and many others — may have difficulty opening a merchant account with traditional financial institutions, they do have other options. This gap in the market has paved the way for companies specializing in providing high-risk credit card services across multiple industries.

If you’ve been unsuccessful in your quest to obtain a “traditional” merchant account, there are several best practices you can apply to try to improve your situation:

1. Do Your Due Diligence

The first step will likely involve conducting research online to find a company that offers payment processing services for businesses like yours. While you’re doing your homework, be aware that there are some companies that don’t deliver on their promises or charge exorbitant fees for their services. Knowing how to avoid them will keep your business protected.

For example, a poorly designed website can be a tipoff that a high-risk merchant account provider will scam you. Aside from examining the website, look at the reviews to see what the company’s customers have to say. If you spot a high ratio of negative-to-positive reviews, you should look elsewhere.

2. Be Aware of Too-Quick Approvals

Just as you should do a thorough vetting of high-risk merchant account providers, you can expect they’ll do the same when reviewing your application. If a company promises fast approvals or requests limited information about you and your business, it’s probably a sign that it’s not a legitimate entity or will charge ridiculously high payment processing fees.

3. Boost Your Credit Score

While you likely won’t need as high of a credit score when applying for a high-risk credit account as when working with a traditional bank, a more favorable score can often result in lower processing fees. Improve your score — and your standing with prospective payment processors — by reducing your debt load, making timely payments to your creditors and avoiding applying for additional credit.

4. Don't Misrepresent Your Situation

While your attempts to find a low-risk merchant account provider may have been frustrating, avoid the temptation to provide false or inaccurate information when applying for a high-risk account. The partner you choose will likely discover the truth when you start receiving credit card payments from your customers. As a result, you could end up on the Terminated Merchant File (TMF) list, making it much more challenging to set up a merchant account in the future.

5. Find a Provider That Works With Multiple Banks

No two high-risk businesses are alike, and the payment processing challenges can vary significantly between companies and industries. By partnering with a merchant account payment provider with access to an extensive network of banks, you can increase your approval odds and are more likely to find the perfect solution for your business.

6. Choose a Company With a High Approval Rate

Although you should be wary of a provider that promises almost immediate approval, you also don’t want to waste time applying with one that turns most businesses down. A reputable high-risk merchant provider that works with multiple banks and has a reasonable minimum credit score standard should be able to work with you. These companies specialize in helping people in your situation and can help you navigate the obstacles on the way to approval.

Getting Approved as a High-Risk Merchant

If you’re seeking to work with a high-risk payment processing company for the first time, you should become familiar with the application and approval process. A few examples of what’s considered a high-risk merchant and what you should be ready for :

Cover Letter

Increase your odds of approval by preparing and submitting a cover letter to the prospective account provider. This document should highlight the most attractive features of your business. For example, the company may view you more favorably if you have extensive experience in your industry or a successful track record as a small business owner. Include information about steps you’re planning to take to ensure smooth, safe credit card transactions, such as taking a proactive approach to fraud monitoring.

Additional Information

Expect any payment processor to order a credit report to verify your credit score and look for red flags regarding your payment history and other areas. Also, you’ll need to provide your tax returns and whatever other financial documentation the provider deems appropriate.

Contract Duration

Sometimes, you have to engage in a longer contract when working with a high-risk payment processor than you would with a traditional bank. While doing so can give you a feeling of security, it might not be beneficial in the long run. If your business’s status changes and you move into a low-risk classification, you’ll still be locked into the higher rates for the remainder of the agreement. Keep this point in mind as you negotiate the length of the term with the provider.

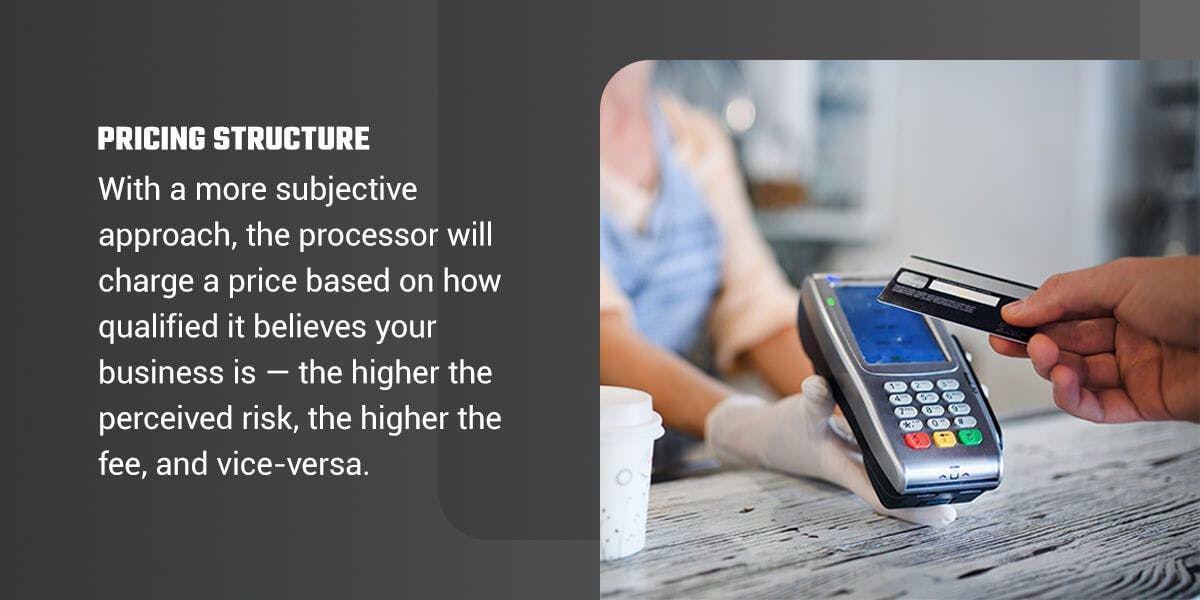

Pricing Structure

In most cases, providers will offer a tiered pricing program to high-risk businesses. With this more subjective approach, the processor will charge a price based on how qualified it believes your business is — the higher the perceived risk, the higher the fee, and vice-versa. This pricing structure is typically more expensive.

Although not as common, some processors may implement an interchange-plus pricing arrangement. It’ll charge a small transaction fee, typically a percentage of the item’s purchase price plus an additional amount that goes to the merchant account provider. This method offers more transparency than the tiered pricing model and is usually more favorable to the business.

Chargeback Fees

As merchant account providers aren’t fond of chargebacks, expect to pay a fee when they occur. These costs can be much more significant for high-risk businesses. If chargebacks are common in your daily operations, you’ll want to know how much they could impact your company’s bottom line. Consider checking with several processors and compare this contract feature.

Reserves

Some high-risk merchant account companies may demand to keep a portion of your business’s credit card sales for protection against excessive chargebacks or fraud. Depending on the agreement, the processor may release the funds back to you if there are no issues. It could also place a specified sum in an escrow account and hold onto the money until it receives an equal amount in processing fees.

In another scenario, the company may charge an additional percentage for each transaction until the reserve fund reaches an amount listed in the contract.

Automatic Renewal

Many payment processors will offer a contract that renews automatically at the end of the designated period. Check the terms closely before signing to determine if this clause exists. Depending on your situation, you might want to explore other merchant account options in the future, meaning that an agreement that rolls over might not be in your best interests. Note whether you need to give the processor advanced notice if you don’t want the contract to continue.

Account Freezing and Termination

The provider could terminate the agreement before the contract expiration date if your business experiences excessive chargebacks, numerous incidents of fraud or other issues. It may also choose to freeze your account for a time, which will prevent your business from accepting credit card or debit card payments. Read the agreement carefully to determine what could jeopardize your standing with the merchant account company and potentially put you out of business.

Contact Zen Payments to Learn More

At Zen Payments, we recognize the challenges that many merchants face when seeking payment processing accounts. Therefore, we focus on serving the needs of high-risk businesses like yours by providing flexible, affordable solutions. We know fully what’s considered a high-risk merchant and we are happy to help!

Zen Payments works with an extensive network of 15 financial institutions, increasing the likelihood of finding the right match for your company. And with our high approval rate — we can help 99% of businesses with a credit score of at least 500 — we can typically say “yes” when other processors say “no.”

Find your Zen by applying for a high-risk merchant account with Zen Payments. Get started by contacting us today to learn more about our credit card processing services and get a quote.